Setting monthly budgets from a rolling forecast Not the Annual Plan

By David Parmenter

Monthly budgets should be set on a quarterly rolling basis. In the last months of the year after the Annual budget has been finalised, we ask budget holders, “What do you really need for the first three months of the new year”.

It is a better practice for the budget holders to set out in less detail the figures for the next five quarters so each quarter, before approving these estimates, management sees the bigger picture six quarters out.

Budget holders are encouraged to spend half the time on getting the detail of the next three months right as these will become targets, on agreement, and the rest of the time on the next five quarters. Each quarter forecast is never a cold start as they have reviewed the forthcoming quarter a number of times. Provided you have appropriate forecasting software, management can do their forecasts very quickly; one airline even does this in three days!! The overall time spent in the four quarterly forecasts during a given year is five weeks.

Most organisations can use the cycle set out below if their year-end falls on a calendar quarter end. Some organisations may wish to stagger the cycle say May, August, November, and February. I will now explain how each forecast works using a June year-end organisation.

The quarterly rolling planning is a process that will revolutionise any organisation whether public or private sector! It removes the four main barriers to success that an annual budgeting process erects. An annual funding regime where budget holders are encouraged to be dysfunctional, a reporting regime base around monthly targets that have no relevance, a three-month period where management are taken away from making money; and the remuneration system based on an annual target.

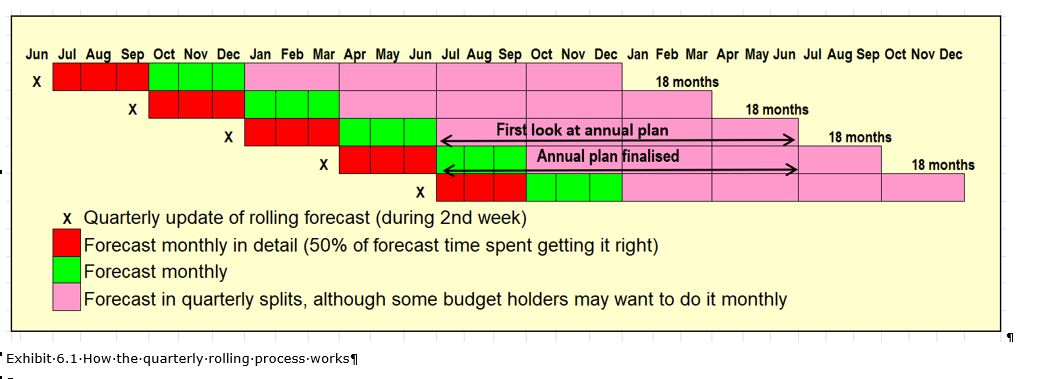

The Quarterly Process (Based on a June Year-End)

Exhibit 6.1 shows how the quarterly rolling process works. The red zone is the next quarters forecast and the most important part to get right. The green zone is the 2nd quarter which is forecast monthly and budget holders are told to get this reasonably right. Budget holders will be re-forecasting this period next quarter in any case. The purple zone is only forecast in quarterly breaks and budget holders are told not to spend too much time second guessing these quarters.

December We forecast out to year-end, with monthly numbers, the remaining period in quarterly breaks. Budget holders obtain approval to spend January to March numbers subject to their forecast still going through the annual budget goal posts. The budget holders at the same time forecast next year’s numbers for the first time. Budget holders are aware of the expected numbers and the first cut is reasonably close. This is a precursor to the annual budget. This forecast is stored in the planning tool.

March We reforecast to year-end and the first quarter of next year with monthly numbers, the remaining period in quarterly breaks. Budget holders obtain approval to spend April to June numbers. The budget holders at the same time revisit the December forecast (the last forecast) of next year’s numbers and fine-tune them for the annual budget. Budget holders know that they will not be getting an annual lump sum funding for their annual budget. The number they supply is for guidance only.

For the annual budget, budget holders will be forecasting their expense codes using an annual number and in quarterly lots for the significant accounts such as personnel costs. Management reviews the annual budget for next year and ensure all numbers are only broken down into quarterly lots and this is stored in a new field in the planning tool called “March 04 forecast”. This is the second look at the year, so the managers have a better understanding. On an ongoing basis you would only need a two-week period to complete this process, if you followed the process set out below..

June We can reforecast the end of June numbers and we should be able to eliminate the frantic activity that is normally associated with the “spend it or lose it” mentality. Budget holders are now also required to forecast the first six months of next year monthly and then on to Dec, 6 quarters on in quarterly numbers. Budget holders obtain approval to spend July to September numbers provided their forecast once again passes through the annual goal posts. This is stored in a new field in the forecasting tool called “e.g., June 07 forecast.” This update process should only take one elapsed week.

September We reforecast the next six months in monthly numbers, and quarterly to March six quarters on. Budget holders obtain approval to spend October to December numbers. This is stored in a new field in the planning tool called “e.g., September 07 forecast”. This update process should only take one elapsed week.

You will find that the four cycles, in a given financial year, take about five weeks, once management is fully conversant with the new forecasting system and processes.

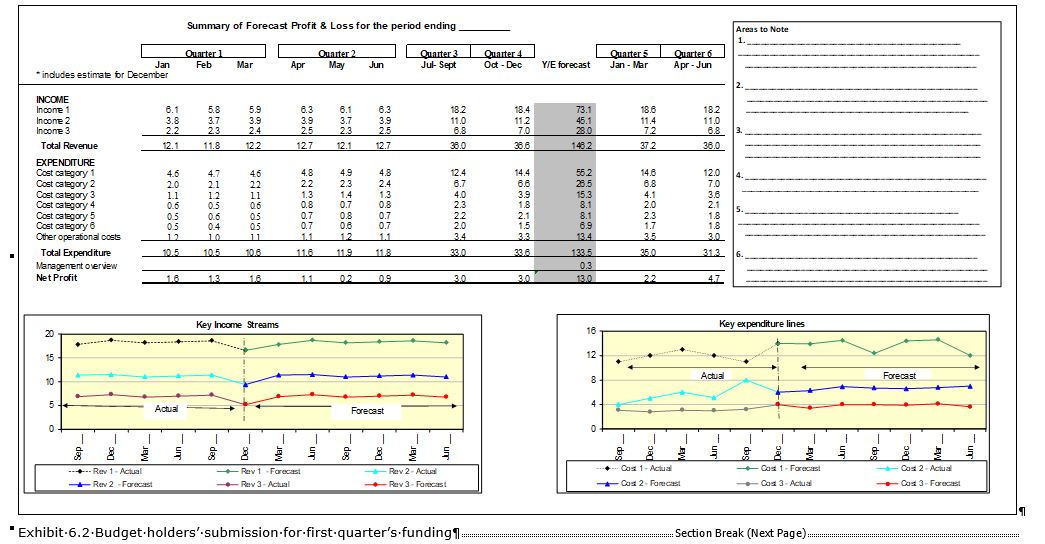

See Exhibits 6.2 for the submission the budget holder would need to do in the last month of the year to request funding for the first quarter. We are finding out how much of the annual budget the budget holder needs. Exhibit 6.3 shows the how quick the update process is

The toolkit is on sale (over 40% discount)

How you establish the Monthly Budgets from a Rolling Forecast is further explored in “An Annual Plan in Two Weeks or Less Toolkit” (Whitepaper + e-templates).

To look inside the toolkit and buy the toolkit

I would recommend you view Bjarte Bogsnes’ presentation on ‘Beyond Budgeting – business agility in practice’

Beyond Budgeting – an agile management model for new business and people – Bjarte Bogsne, at USI

Also read:

https://review.firstround.com/Annual-Planning-is-Killing-Your-Growth-Try-This-Instead

https://hbr.org/2006/01/stop-making-plans-start-making-decisions

https://corporatefinanceinstitute.com/resources/knowledge/finance/beyond-budgeting/

[i] Jeremy Hope and Robin Fraser, Beyond Budgeting: How Managers Can Break Free from the Annual Perfo